A personal loan is a lump sum of money you borrow from a bank, credit union, or online lender and repay in fixed monthly payments. Unlike a mortgage or car loan, most personal loans are unsecured, meaning you don’t need to put up collateral like a house or vehicle.

People use personal loans for many reasons—to consolidate credit card debt, cover medical expenses, or fund home improvements. Since they come with fixed interest rates and repayment terms, they can be a smart way to manage large expenses.

Lenders include traditional banks, credit unions, and online platforms that offer fast approvals and flexible terms. In this guide, we’ll break down how personal loans work, their common uses, and the best places to get one so you can make the right financial choice.

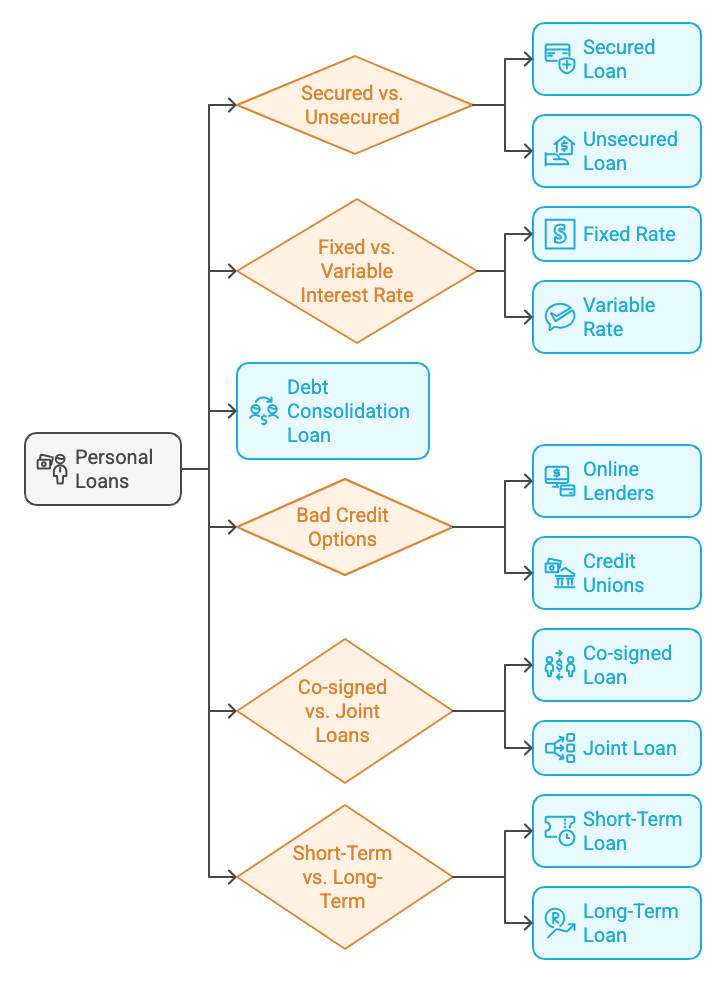

Types of Personal Loans

Personal loans come in different forms, each suited for specific financial situations. Understanding the differences can help you choose the best option based on your needs, credit score, and repayment ability.

Secured vs. Unsecured Personal Loans

A key distinction between personal loans is whether they are secured or unsecured. Here’s how they compare:

| Feature | Secured Personal Loan | Unsecured Personal Loan |

| Requires Collateral | Yes (home, car, savings) | No collateral required |

| Interest Rates | Lower | Higher |

| Approval Requirements | Easier if collateral is provided | Based on credit score and income |

| Loan Amount | Higher limits | Lower limits |

| Risk | If you default, the lender can seize the collateral | No collateral at risk, but missed payments harm credit score |

Which to Choose?

- Choose a secured loan if you want lower interest rates and have collateral to back the loan.

- Choose an unsecured loan if you prefer less risk and have a strong credit score to qualify for good rates.

Fixed vs. Variable Interest Rate Loans

When taking out a personal loan, you’ll also need to decide between a fixed or variable interest rate.

- Fixed Interest Rate: The rate stays the same throughout the loan term, meaning predictable payments.

- Variable Interest Rate: The rate can fluctuate based on market conditions, meaning payments can increase or decrease over time.

Which is better?

- Fixed rates are best for those who want stability and predictability in payments.

- Variable rates might be an option if you expect rates to drop and can handle occasional fluctuations.

Debt Consolidation Loans (When They Make Sense)

A debt consolidation loan is designed to combine multiple debts into one—usually with a lower interest rate. This can be a good option if:

- You have multiple high-interest credit card balances.

- You want a single monthly payment instead of juggling multiple bills.

- Your new loan has a lower APR, saving you money over time.

However, it may not be ideal if the loan fees are high or the new interest rate is not significantly lower than what you’re currently paying.

Bad Credit Personal Loans (Best Options for Low Credit Scores)

If your credit score is below 600, you may find it harder to qualify for traditional loans. However, some lenders specialize in bad credit personal loans.

Options include:

- Online lenders that cater to lower credit scores.

- Credit unions, which often offer more flexible approval criteria.

- Secured loans, where collateral can help offset a low score.

- Co-signed loans, where someone with good credit guarantees your loan.

Tip: If you have bad credit, compare multiple lenders and check for hidden fees or excessively high APRs before committing.

Co-signed and Joint Personal Loans

If you have trouble qualifying for a personal loan on your own, you might consider a co-signed or joint loan.

- Co-signed Loan: A second person (co-signer) agrees to be responsible for the loan if the primary borrower fails to pay.

- Joint Loan: Both borrowers share equal responsibility for the loan and payments.

Best for:

- Borrowers with low credit scores who need help getting approved.

- Those who want better interest rates by using a co-signer with a strong credit profile.

However, co-signers take on risk—if the borrower misses payments, the co-signer’s credit score can be affected.

Short-Term vs. Long-Term Personal Loans

The length of your loan term can impact your monthly payments and total interest paid.

| Term Length | Monthly Payment | Total Interest Paid |

| Short-Term (1-3 years) | Higher payments | Less interest overall |

| Long-Term (4-7 years) | Lower payments | More interest overall |

Which should you choose?

- Short-term loans are ideal if you want to pay off debt quickly and save on interest.

- Long-term loans provide lower monthly payments but cost more in interest over time.

Choosing the right type of personal loan depends on your financial situation and goals. By understanding the differences, you can secure the best terms, minimize risks, and ensure affordable repayment.

How to Qualify & Apply for a Personal Loan

Applying for a personal loan requires meeting specific eligibility criteria and understanding how lenders evaluate your application. This section breaks down what you need to qualify, how your credit score impacts approval, and the step-by-step process to apply for a loan.

Eligibility Criteria Explained

Lenders evaluate several factors to determine your ability to repay a loan. Here’s what they typically look for:

- Credit Score: A minimum of 600+ is generally required, but scores above 700 secure the best interest rates.

- Debt-to-Income (DTI) Ratio: Lenders prefer a DTI below 40%—this shows you have enough income to cover new debt.

- Stable Income & Employment: Proof of consistent income through pay stubs, tax returns, or bank statements.

- U.S. Residency & Age: Must be 18+ years old and have a U.S. bank account.

Required Documents Checklist:

- Government-issued ID (Driver’s License, Passport, or Social Security Number)

- Proof of Income (Recent Pay Stubs, Tax Returns, or Bank Statements)

- Employer Information & Contact Details

- Proof of Address (Utility Bill, Lease Agreement, or Mortgage Statement)

How Credit Scores Affect Your Approval & Interest Rate

Your credit score is one of the biggest factors in getting approved and securing a low interest rate. Here’s how it affects your loan terms:

| Credit Score Range | Approval Chances | Typical Interest Rate |

| 750+ (Excellent) | Very High | 6% – 10% (Best rates) |

| 700 – 749 (Good) | High | 10% – 15% |

| 650 – 699 (Fair) | Moderate | 15% – 20% |

| 600 – 649 (Poor) | Low | 20% – 30% |

| Below 600 (Bad Credit) | Very Low | 30%+ (Limited options, high fees) |

Tip: If your credit score is below 650, consider a co-signer, secured loan, or improving your credit before applying.

Debt-to-Income Ratio & Its Impact on Loan Approval

Your Debt-to-Income Ratio (DTI) compares your monthly debt payments to your gross income. Lenders use this to assess how well you manage debt.

DTI Formula:

DTI = (Total Monthly Debt Payments ÷ Gross Monthly Income) × 100

DTI Ranges & Approval Odds:

| DTI Range | Approval Chances |

| Below 30% | Very High |

| 30% – 40% | Good |

| 40% – 50% | Moderate (May need higher credit score) |

| 50%+ | Low (Consider paying down debt first) |

Tip: Reducing your DTI before applying increases your approval chances and helps secure better loan terms.

Pre-Qualification vs. Hard Inquiry – Which One to Choose?

Before applying, you may see an option to pre-qualify. This lets you check potential loan offers without affecting your credit score.

| Feature | Pre-Qualification | Hard Inquiry (Full Application) |

| Credit Impact | No impact (soft check) | Can temporarily lower score |

| Approval Guarantee? | No, just an estimate | Yes, if approved |

| Shows Interest Rate? | Yes | Yes |

| When to Use? | Shopping for best rates | Ready to officially apply |

Tip: Always pre-qualify with multiple lenders before applying for a loan to compare rates and avoid unnecessary credit inquiries.

Step-by-Step Application Process (With Lender Comparison Table)

Applying for a personal loan is straightforward, but choosing the right lender matters.

Step-by-Step Process:

- Check Your Credit Score – Use free services like Experian or Credit Karma to know where you stand.

- Calculate Your Budget – Determine how much you can afford in monthly payments.

- Pre-Qualify with Multiple Lenders – Compare offers without hurting your credit.

- Compare Loan Terms – Look at APR, fees, repayment terms, and approval time.

- Gather Required Documents – Make sure you have income proof, ID, and bank details.

- Submit Your Application – Complete the online or in-person application.

- Review and Accept the Offer – Read the fine print before signing.

- Receive Your Funds – Some lenders offer same-day funding, while others take 1-5 business days.

Lender Comparison Table:

| Lender | APR Range | Minimum Credit Score | Funding Time |

| SoFi | 7.99% – 23.43% | 680+ | 1-3 days |

| LightStream | 6.99% – 22.99% | 660+ | Same day |

| Upgrade | 8.49% – 35.99% | 580+ | 1 day |

| Upstart | 6.7% – 35.99% | 600+ | 1-2 days |

| Avant | 9.95% – 35.99% | 580+ | 1 day |

Tip: Choose a lender with the lowest APR and minimal fees based on your credit profile.

Getting approved for a personal loan depends on your credit score, income, and DTI ratio. Always compare multiple lenders, pre-qualify before applying, and ensure you can handle the monthly payments. Following these steps will help you secure the best loan terms and avoid unnecessary costs.

Costs, Fees & Interest Rates

Understanding the costs associated with a personal loan is crucial to making a financially sound decision. Many borrowers focus only on the interest rate, but hidden fees, loan terms, and APR can significantly impact the total cost of borrowing. This section will break down how APR works, the differences between fixed and variable rates, common fees to watch for, and tips on securing the lowest interest rate possible.

Before applying for a loan, use our Personal Loan Calculator to estimate your monthly payments and total loan cost based on different interest rates and loan terms.

How APR (Annual Percentage Rate) Works

The Annual Percentage Rate (APR) represents the total cost of borrowing, including both the interest rate and lender fees. Unlike a simple interest rate, APR gives a more accurate picture of the total loan cost.

Example of How APR Affects Loan Cost

| Loan Amount | Interest Rate | APR | Monthly Payment (3-year term) | Total Repayment Cost |

| $10,000 | 8.99% | 9.49% | $318 | $11,448 |

| $10,000 | 12.99% | 14.49% | $343 | $12,348 |

| $10,000 | 20.99% | 22.49% | $390 | $14,040 |

Lower APR = Lower total loan cost.

Tip: Always compare APR, not just interest rates, as some lenders charge higher fees that increase the actual borrowing cost.

Fixed vs. Variable Interest Rates – Pros & Cons

Borrowers can choose between fixed-rate and variable-rate personal loans. Each has its own advantages and risks.

| Feature | Fixed Interest Rate | Variable Interest Rate |

| Rate Stability | Stays the same for the entire loan term | Changes based on market fluctuations |

| Predictability | Monthly payments remain constant | Payments may increase or decrease |

| Risk Level | Low risk | Higher risk if rates rise |

| Best For | Those who prefer stability and predictable payments | Those who can handle fluctuations and want to take advantage of potential rate drops |

Tip: If interest rates are expected to rise, fixed-rate loans are the safer option. If rates are high but expected to drop, a variable-rate loan may be worth considering.

Breakdown of Hidden Fees

Many lenders advertise low interest rates but offset costs through hidden fees. Here are the most common charges:

1. Origination Fees

- Typically 1% – 6% of the loan amount.

- Deducted upfront from your loan balance.

- Example: A $10,000 loan with a 3% origination fee means you only receive $9,700, but you still repay the full $10,000 plus interest.

2. Prepayment Penalties

- Some lenders charge a fee for paying off a loan early.

- Why? Lenders lose interest income when borrowers pay off loans ahead of schedule.

- Example: A $5,000 loan with a 2% prepayment fee costs you $100 if you pay it off early.

3. Late Payment Fees

- Can range from $25 to $50 per missed payment.

- Some lenders charge a percentage of the overdue amount instead.

- Tip: Set up automatic payments to avoid late fees.

4. Insufficient Funds Fee (NSF Fee)

- If your payment is rejected due to insufficient funds, lenders may charge $25 – $35 per failed attempt.

Tip: Always check the lender’s fee schedule before signing a loan agreement.

How to Get the Lowest Interest Rate Possible

Getting the lowest interest rate requires planning and strategy. Here are actionable steps to secure the best deal:

1. Improve Your Credit Score

| Credit Score Range | Typical APR |

| 750+ (Excellent Credit) | 6% – 10% |

| 700 – 749 (Good Credit) | 10% – 15% |

| 650 – 699 (Fair Credit) | 15% – 25% |

| 600 – 649 (Poor Credit) | 25%+ |

Steps to Improve Credit Score Before Applying:

- Pay off existing debts to lower credit utilization.

- Avoid applying for multiple loans at once (reduces hard inquiries).

- Dispute errors on your credit report to improve your score.

2. Compare Multiple Lenders Before Applying

| Lender | APR Range | Min. Credit Score | Funding Time |

| LightStream | 6.99% – 22.99% | 660+ | Same day |

| SoFi | 7.99% – 23.43% | 680+ | 1-3 days |

| Upgrade | 8.49% – 35.99% | 580+ | 1 day |

| Upstart | 6.7% – 35.99% | 600+ | 1-2 days |

| Avant | 9.95% – 35.99% | 580+ | 1 day |

Tip: Pre-qualify with multiple lenders to compare APR, loan terms, and hidden fees before committing.

3. Consider a Co-Signer

- Adding someone with good credit can lower your interest rate.

- A co-signer shares loan responsibility, meaning missed payments affect both credit scores.

4. Choose a Shorter Loan Term

- Shorter terms (3-5 years) = Lower interest rates.

- Longer terms (6-7 years) = More interest paid over time.

Tip: If monthly payments are affordable, opt for a shorter loan term to save on interest.

Many borrowers focus only on interest rates, but understanding APR, hidden fees, and loan terms ensures you get the best possible deal. Always shop around, improve your credit score, and negotiate loan terms to minimize borrowing costs.

Managing & Repaying a Personal Loan

Taking out a personal loan is just the first step—managing repayment effectively ensures you stay on track financially while minimizing costs. This section provides actionable strategies for repayment, credit score impact, handling missed payments, and paying off your loan early without penalties.

Best Strategies for Repayment

The way you repay your loan can significantly affect how much interest you pay and how quickly you become debt-free. Here are proven strategies to manage repayment efficiently:

1. Bi-Weekly Payments (Accelerated Repayment)

- Instead of 12 monthly payments, make half-payments every two weeks.

- Over a year, this results in 26 half-payments (or 13 full payments) instead of 12.

- Effect: You make one extra payment per year, reducing loan duration and interest costs.

2. Round Up Your Payments

- Round up your monthly payment to the nearest $50 or $100.

- Example: If your payment is $267, round it to $300—this small increase accelerates payoff.

3. Make Extra Payments When Possible

- Apply bonuses, tax refunds, or extra income toward your loan.

- Always check for prepayment penalties before making large additional payments.

4. Automate Payments to Avoid Late Fees

- Set up automatic payments to ensure on-time payments, avoiding late fees and negative credit impact.

- Some lenders offer interest rate discounts (0.25% – 0.50%) for using autopay.

Tip: Even a small extra payment each month can shave months or even years off your loan term.

How Personal Loans Impact Your Credit Score

Your personal loan can either help or hurt your credit score, depending on how you manage repayment.

| Credit Factor | Positive Impact | Negative Impact |

| On-Time Payments | Boosts credit score over time | Late payments hurt score significantly |

| Credit Mix | Diversifies credit profile, improving score | No major negative impact |

| Credit Utilization | Lower debt-to-credit ratio improves score | Higher outstanding debt can lower score |

| Hard Inquiries | Minor, temporary score drop | Too many applications reduce score |

Tip: Paying on time every month is the most important factor for keeping your credit score high.

What Happens If You Miss a Payment?

Missing a payment can lead to fees, collection actions, and credit damage. Here’s what typically happens:

1. Grace Period (1-15 Days Late)

- Some lenders offer a grace period before charging late fees.

- Contact your lender immediately if you anticipate a late payment.

2. Late Fees & Credit Score Drop (15-30 Days Late)

- Late fees (typically $25-$50) apply.

- Payments over 30 days late are reported to credit bureaus, lowering your score by 50+ points.

3. Collections & Legal Action (60-90 Days Late)

- Loan defaults may lead to debt collection agencies contacting you.

- Repeated missed payments may result in lawsuits, wage garnishment, or asset seizure for secured loans.

Tip: If you can’t make a payment, contact your lender immediately—many offer hardship programs to delay or adjust payments.

Strategies for Paying Off a Loan Early (Without Penalties)

Paying off a loan early saves money on interest, but some lenders charge prepayment penalties. Here’s how to pay off a loan without unnecessary fees:

- Choose a Loan Without Prepayment Penalties: Before taking a loan, check the fine print for early payoff fees.

- Apply Extra Payments Toward Principal: Some lenders apply extra payments to future interest—request that extra payments go directly to principal instead.

- Refinance for a Shorter Term: If your credit improves, refinance your loan to a lower rate or shorter term to save on interest.

- Use Windfalls to Pay Down Debt: Apply bonuses, tax refunds, or side income toward your loan balance.

Tip: Even paying an extra $50 per month can save hundreds or thousands over the life of your loan.

Managing your personal loan repayment wisely can help you pay off debt faster, avoid penalties, and maintain a strong credit score. Use smart repayment strategies like bi-weekly payments, rounding up, and automating payments to stay on track and minimize interest costs.

Alternatives to Personal Loans (When NOT to Get One)

Personal loans are useful, but they aren’t always the best borrowing option. Depending on your financial situation, alternatives like home equity loans, 0% APR credit cards, peer-to-peer lending, borrowing from family, or even a personal line of credit may be smarter choices. Below, we compare these options so you can make the best decision for your needs.

Home Equity Loans vs. Personal Loans

If you own a home, you may qualify for a home equity loan or home equity line of credit (HELOC) instead of a personal loan.

| Feature | Home Equity Loan | Personal Loan |

| Collateral Required? | Yes (Your home) | No |

| Interest Rates | Lower (5%-10%) | Higher (6%-36%) |

| Loan Amount | Higher (up to 80% of home equity) | Lower (based on credit score & income) |

| Approval Speed | Slower (2-4 weeks) | Faster (Same-day to a few days) |

| Risk | Foreclosure if unpaid | No asset risk |

When to Choose a Home Equity Loan:

- You need a large loan at a lower interest rate.

- You have strong home equity and can afford longer repayment terms.

When to Choose a Personal Loan:

- You don’t want to use your home as collateral.

- You need faster funding.

0% APR Credit Cards vs. Personal Loans for Debt Consolidation

A 0% APR credit card can be an alternative for consolidating high-interest debt, especially if you can pay off the balance before the introductory period ends.

| Feature | 0% APR Credit Card | Personal Loan |

| Best For | Short-term borrowing (0% APR period) | Long-term, fixed payments |

| Interest Rate | 0% for 6-24 months, then 15%-25% | Fixed 6%-36% |

| Repayment Term | Flexible | Fixed (1-7 years) |

| Loan Amount | Limited to credit limit | Higher borrowing limits |

When to Choose a 0% APR Credit Card:

- You can pay off the balance before the 0% APR period ends.

- You only need a small amount of credit.

When to Choose a Personal Loan:

- You need a structured repayment plan.

- You’re consolidating a large amount of debt.

Peer-to-Peer Lending vs. Traditional Loans (Is P2P Better?)

Peer-to-peer (P2P) lending platforms like LendingClub and Prosper connect borrowers with investors who fund loans. These can be an alternative to traditional bank loans.

| Feature | Peer-to-Peer Loan | Traditional Bank Loan |

| Approval Process | More flexible | Stricter credit checks |

| Interest Rates | Varies based on risk profile | Standardized rates |

| Funding Speed | 3-7 days | 1-5 days |

| Best For | Borrowers with fair credit who can’t qualify at banks | Those who prefer established financial institutions |

When to Choose P2P Lending:

- You have a fair credit score and want more approval flexibility.

- You’re comfortable borrowing from individual investors rather than banks.

When to Choose a Traditional Loan:

- You prefer a regulated financial institution.

- You want structured repayment terms with a fixed rate.

Borrowing from a 401(k) or IRA – A Risky Alternative?

If you have retirement savings, borrowing from a 401(k) or IRA might seem like a quick way to access funds—but it comes with risks.

| Feature | 401(k) Loan | IRA Withdrawal |

| Repayment Required? | Yes (usually within 5 years) | No repayment, but penalties apply |

| Taxes & Penalties? | No penalties if repaid on time | 10% early withdrawal penalty (before age 59½) |

| Impact on Retirement? | Reduces growth of retirement savings | Permanently reduces retirement funds |

When to Consider Borrowing from a 401(k) or IRA:

You have no other borrowing options and can repay quickly.

When to Avoid:

- You risk losing retirement savings that could grow significantly over time.

- You face penalties and taxes for early withdrawals.

Tip: Only use this option as a last resort.

Personal Line of Credit vs. Traditional Personal Loan

A personal line of credit (PLOC) offers flexibility similar to a credit card, while a traditional personal loan provides a lump sum with fixed payments.

| Feature | Personal Line of Credit | Personal Loan |

| Loan Type | Revolving credit | Lump sum |

| Best For | Ongoing, unpredictable expenses | One-time, large expense |

| Interest Rate | Variable | Fixed |

| Repayment Structure | Pay interest only on what you use | Fixed monthly payments |

When to Choose a Personal Line of Credit:

- You don’t need all the money upfront but want access when needed.

- You can handle variable interest rates.

When to Choose a Personal Loan:

- You need a one-time lump sum with a structured repayment plan.

- You want predictable, fixed payments.

Borrowing from Family or Friends – A Flexible But Risky Option

Turning to family or close friends for a loan can help avoid interest and credit checks, but it can also strain relationships.

| Feature | Family/Friend Loan | Personal Loan |

| Credit Check? | No | Yes |

| Interest Rate | Low or none | 6%-36% |

| Approval Process | Based on trust | Based on financial history |

| Legal Protection? | None unless documented | Governed by loan contracts |

When to Borrow from Family/Friends:

- You need a small loan without going through a lender.

- You and the lender trust each other and can agree on repayment terms.

When to Avoid:

- If there’s a chance of misunderstanding or relationship strain.

- If you can’t commit to repayment and risk damaging personal ties.

Tip: Always document loan terms in writing to avoid disputes.

Personal loans are useful, but they’re not always the best option. Depending on your needs, a home equity loan, 0% APR credit card, peer-to-peer loan, personal line of credit, or even borrowing from family could be better alternatives. Always compare interest rates, risks, and repayment terms before making a final decision.

FAQ & Final Tips for Borrowers

When considering a personal loan, many borrowers have important questions about eligibility, approval speed, and avoiding scams. This section answers the most frequently asked questions and provides a final loan comparison table to help you choose the best option.

What’s the Best Personal Loan for Bad Credit?

Borrowers with low credit scores (below 600) may struggle to qualify for a personal loan with favorable terms. However, some lenders specialize in bad credit loans, offering higher approval odds with reasonable terms.

Top Lenders for Bad Credit Borrowers

| Lender | APR Range | Min. Credit Score | Loan Amounts | Funding Time |

| Upgrade | 8.49% – 35.99% | 580+ | $1,000 – $50,000 | 1 day |

| Upstart | 6.7% – 35.99% | 600+ | $1,000 – $50,000 | 1-2 days |

| Avant | 9.95% – 35.99% | 580+ | $2,000 – $35,000 | 1 day |

| LendingPoint | 7.99% – 35.99% | 580+ | $2,000 – $36,500 | Next day |

| OneMain Financial | 18.00% – 35.99% | No minimum | $1,500 – $20,000 | Same day |

Tip: If you have bad credit, consider a co-signer or a secured loan to improve approval odds and lower interest rates.

Can I Get a Personal Loan Without a Job?

Yes, but it’s more challenging. Most lenders require proof of income, but alternatives exist:

- Alternative Income Sources: Lenders may accept social security, alimony, rental income, or freelance earnings.

- Using a Co-Signer: A co-signer with stable income improves your approval chances.

- Secured Loan Option: Some lenders offer secured personal loans backed by collateral (car, savings, etc.).

Tip: If you’re unemployed, avoid payday loans and predatory lenders that charge excessive fees and high-interest rates.

How Fast Can I Get Approved?

Approval and funding speed depend on the lender. Some online lenders offer same-day funding, while banks and credit unions may take several days.

Not sure how much you can afford? Try our Personal Loan Calculator to estimate your monthly payments before choosing a lender.

| Lender Type | Approval Time | Funding Speed |

| Online Lenders (e.g., Upstart, SoFi, Upgrade) | Instant to 1 day | Same day to 2 days |

| Credit Unions | 1-3 days | 2-5 days |

| Traditional Banks | 2-5 days | 3-7 days |

Tip: If you need urgent funding, choose a lender offering instant pre-approval and same-day funding.

What Should I Watch Out for to Avoid Scams?

Unfortunately, some lenders take advantage of borrowers with hidden fees, misleading terms, or outright fraud.

Red Flags of Predatory Lenders:

- Upfront Fees: Legitimate lenders never require payment before approval.

- Guaranteed Approval: No reputable lender guarantees a loan without reviewing credit and income.

- No Physical Address: If a lender lacks a verifiable business address and phone number, it’s a major red flag.

- Pressuring You to Sign Quickly: Scammers push borrowers into rushed decisions without fully reviewing terms.

- Unclear or Vague Loan Terms: If fees, repayment terms, or interest rates are hard to find or understand, walk away.

Tip: Check the lender’s Better Business Bureau (BBB) rating and read online reviews before applying.

Final Loan Comparison Table: Best Options by Category

Here’s a quick comparison of the best personal loans based on specific borrower needs:

| Best For | Lender | APR Range | Loan Amounts | Min. Credit Score | Funding Time |

| Lowest APR | LightStream | 6.99% – 22.99% | $5,000 – $100,000 | 660+ | Same day |

| Bad Credit | Upgrade | 8.49% – 35.99% | $1,000 – $50,000 | 580+ | 1 day |

| Fastest Approval | Upstart | 6.7% – 35.99% | $1,000 – $50,000 | 600+ | Same day |

| No Fees | SoFi | 7.99% – 23.43% | $5,000 – $100,000 | 680+ | 1-3 days |

| Small Loans | OneMain Financial | 18.00% – 35.99% | $1,500 – $20,000 | No minimum | Same day |

Tip: Always compare APR, loan terms, fees, and funding speed to choose the best option.

Final Tips for Borrowers

Before taking out a personal loan, consider these expert-backed tips:

- Compare Multiple Lenders: Pre-qualify with at least three lenders to find the best rate.

- Check the Fine Print: Watch for hidden fees, prepayment penalties, and misleading loan terms.

- Borrow Only What You Need: Avoid over-borrowing just because you qualify for a higher amount.

- Use a Loan Calculator: Estimate your monthly payments before applying.

- Improve Your Credit Score Before Applying: Even a 20-point increase can significantly lower your interest rate.

- Avoid Payday Loans & Predatory Lenders: These loans have extremely high APRs (300%+), leading to a cycle of debt.

By following these guidelines, you can secure the best personal loan while minimizing costs and avoiding scams. Always do your research, compare options, and ensure you can comfortably afford repayments before signing any agreement.